During the last quarter, investors have been risk-averse, mainly sticking to conservative investments. The decreased risk appetite owes to inflation and increasing interest rates. The unfavorable climate has reduced the valuation of some profitable investment stocks, such as ETSY.

ETSY is a well-run company and a reasonable investment for a long-term investor. The company's unique business model is increasingly taking it to the top of the game. ETSY has become the top e-commerce go-to for consumers in many categories.

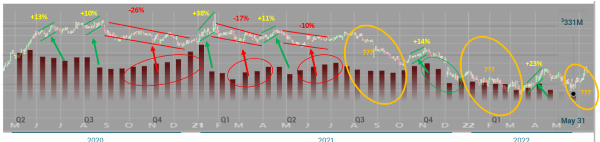

Why Etsy as a top growth long stock plummeted in 2021

ETSY stock plummeted by close to 75% in late 2021. The plummet was caused by slow growth in the post-pandemic market. During the pandemic, the company's traffic and sales increased as more people shopped online.

It also made some key acquisitions, which boosted Revenue. However, things turned post-pandemic at the end of the year, when total dependence on e-commerce was reduced. Revenue by the end of last year increased by a mere 35%, compared to the 111% surge of 2020.

EBITDA margins also declined in Q1 2022, leading to low-margin Revenue. Moreover, its stock was overvalued by at least 120 times the estimated earnings in 2021. ETSY would have been impossible to sustain the overvaluation, as interest rates have significantly increased to date.

Why you should consider Etsy as an investment option

I believe most of ETSY’s stock and financial challenges are temporary. This is due to the pre-pandemic indicators. A survey conducted by the Harris poll estimated that 75% of e-commerce shoppers in America shopped for unique gifts.

It is expected that ETSY will profit from this general shopper preference, as they specialize in unique and handmade products. ETSY is more appealing to Gen Z shoppers, especially after the acquisition of Depop, which retailing second-hand clothes to early 20s shoppers.

ETSY may soon come to the top compared to its main competitors, such as Amazon, because of its hold on this particular niche. The company has a reputable engagement rate, which is critical in retaining and attracting new customers.

ETSY is yet to explore the overseas market to its full potential; therefore, there is room for growth. In 2021, 43% of its gross merchandise sales were from overseas. It will expand in Latin America and Southeast Asia in the coming years.

The general analysts' outlook for Revenue is 19% by the end of next year. The current projection ratios are more sustainable than they stood at in 2021.

Financial metrics

ETSY has a fixed cost structure that ensures net income increases at a higher rate than sales. This metric gives it a significant operating advantage. In 2015, the company reported an annual loss of $54 million.

It is impressive that good management has turned the company into the profitable enterprise it is today.

The company generates a high volume of cash because of its 'no inventory' business model. By only connecting buyers and sellers, the company frees up its capital.

Fundamental Analysis

• 11.64% return on assets against an industry average of -6.04%

• A profit margin of 18.49% against an industry average of -3.74%

• Return on Equity of 64.39% against an industry average of 12.41%

• A Low PEG ratio indicates that ETSY is likely undervalued

However, ETSY may be more expensive than its industry peers may. This takes into account the difference between its enterprise value and EBITDA. With a ratio of 11.22, higher than most industry peers.

Growth Rating

• Earnings per share growth of 63.26%, consistently over the last five years

• Expected growth of 25.90% of EPS over the next five years

The projection indicates that investors will earn more as per their investment and at a very high margin.

• Growth in Revenue of 15.11% in the last year and an average gain of 44.87% over the previous five years.

• The projected outlook for the next five years is 17.43% for revenue growth.

Takeaway

The expected growth of ETSY may not be seen immediately, as investors are still unsure of the current slowdown. However, the future looks bright, as ETSY has proven how it plans to remain relevant in the coming years through metrics.

The company will likely get ahead of rival e-commerce giants as it differentiates itself with a defensible niche. By focusing on handmade and unique crafty items, ETSY will probably gain traction in the future as more people seek customized products.

Its planned expansion in South Asia and European counties such as Germany, Australia, and France shows excellent promise to tap into a new market. The company has the advantage of its ability to offer clients a unique experience.

As an intelligent investor, don’t take the current trend of ETSY stock at face value and be tempted to sell or avoid buying. The company has a feasible business plan, a stable financial base, and great returns are expected in the future. Take advantage of the current slowdown to buy and hold.

During the last quarter, investors have been risk-averse, mainly sticking to conservative investments. The decreased risk appetite owes to inflation and increasing interest rates. The unfavorable climate has reduced the valuation of some profitable investment stocks, such as ETSY.

ETSY is a well-run company and a reasonable investment for a long-term investor. The company's unique business model is increasingly taking it to the top of the game. ETSY has become the top e-commerce go-to for consumers in many categories.

Why Etsy as a top growth long stock plummeted in 2021

ETSY stock plummeted by close to 75% in late 2021. The plummet was caused by slow growth in the post-pandemic market. During the pandemic, the company's traffic and sales increased as more people shopped online.

It also made some key acquisitions, which boosted Revenue. However, things turned post-pandemic at the end of the year, when total dependence on e-commerce was reduced. Revenue by the end of last year increased by a mere 35%, compared to the 111% surge of 2020.

EBITDA margins also declined in Q1 2022, leading to low-margin Revenue. Moreover, its stock was overvalued by at least 120 times the estimated earnings in 2021. ETSY would have been impossible to sustain the overvaluation, as interest rates have significantly increased to date.

Why you should consider Etsy as an investment option

I believe most of ETSY’s stock and financial challenges are temporary. This is due to the pre-pandemic indicators. A survey conducted by the Harris poll estimated that 75% of e-commerce shoppers in America shopped for unique gifts.

It is expected that ETSY will profit from this general shopper preference, as they specialize in unique and handmade products. ETSY is more appealing to Gen Z shoppers, especially after the acquisition of Depop, which retailing second-hand clothes to early 20s shoppers.

ETSY may soon come to the top compared to its main competitors, such as Amazon, because of its hold on this particular niche. The company has a reputable engagement rate, which is critical in retaining and attracting new customers.

ETSY is yet to explore the overseas market to its full potential; therefore, there is room for growth. In 2021, 43% of its gross merchandise sales were from overseas. It will expand in Latin America and Southeast Asia in the coming years.

The general analysts' outlook for Revenue is 19% by the end of next year. The current projection ratios are more sustainable than they stood at in 2021.

Financial metrics

ETSY has a fixed cost structure that ensures net income increases at a higher rate than sales. This metric gives it a significant operating advantage. In 2015, the company reported an annual loss of $54 million.

It is impressive that good management has turned the company into the profitable enterprise it is today.

The company generates a high volume of cash because of its 'no inventory' business model. By only connecting buyers and sellers, the company frees up its capital.

Fundamental Analysis

• 11.64% return on assets against an industry average of -6.04% • A profit margin of 18.49% against an industry average of -3.74% • Return on Equity of 64.39% against an industry average of 12.41% • A Low PEG ratio indicates that ETSY is likely undervalued

However, ETSY may be more expensive than its industry peers may. This takes into account the difference between its enterprise value and EBITDA. With a ratio of 11.22, higher than most industry peers.

Growth Rating

• Earnings per share growth of 63.26%, consistently over the last five years • Expected growth of 25.90% of EPS over the next five years The projection indicates that investors will earn more as per their investment and at a very high margin. • Growth in Revenue of 15.11% in the last year and an average gain of 44.87% over the previous five years. • The projected outlook for the next five years is 17.43% for revenue growth.

Takeaway

The expected growth of ETSY may not be seen immediately, as investors are still unsure of the current slowdown. However, the future looks bright, as ETSY has proven how it plans to remain relevant in the coming years through metrics.

The company will likely get ahead of rival e-commerce giants as it differentiates itself with a defensible niche. By focusing on handmade and unique crafty items, ETSY will probably gain traction in the future as more people seek customized products.

Its planned expansion in South Asia and European counties such as Germany, Australia, and France shows excellent promise to tap into a new market. The company has the advantage of its ability to offer clients a unique experience.

As an intelligent investor, don’t take the current trend of ETSY stock at face value and be tempted to sell or avoid buying. The company has a feasible business plan, a stable financial base, and great returns are expected in the future. Take advantage of the current slowdown to buy and hold.